This month in crypto: the pope, the anti-pope and the pirate

We could be about to see a new crypto superpower emerge and eclipse America’s long-standing tech dominance. Here’s what you need to know.

If you drop an object from a height it will keep on accelerating until it reaches terminal velocity.

It will then maintain that speed until it hits the ground.

The terminal velocity of a person is around 120 mph.

The terminal velocity of crypto seems to be much, much faster than that.

Every month for the last year or so more and more major stories are coming out. And their pace is only accelerating.

Last month I said, “there are so many developments this month that it’s like we’re back in 2017 again.”

Well, this month I have nothing to compare it to. We’re in unchartered territory.

It’s impossible to cover everything that’s gone on this month. But there is one overarching theme that we simply cannot ignore.

So that’s what this month’s issue will centre on.

There is also some crazy stuff happening with IOTA, which somehow hasn’t really blown up yet. I’ll cover that in the specific crypto section a bit further down.

If you hold IOTA, or are thinking about holding IOTA, you won’t want to miss it.

Okay, so what’s this month’s major theme?

I’ll give you a clue… it’s a theme that more than anything else is going to determine the fate of crypto in the short, medium, and long term.

And it’s also a theme that we the people get absolutely no say in.

Governments around the world are gunning for crypto with both barrels

First China banned crypto, then India banned crypto.

Then India didn’t ban crypto.

Then China didn’t ban crypto.

But then China definitely did ban crypto.

Then India banned crypto again.

And now India isn’t really banning crypto, it’s just banning all crypto its government doesn’t create.

Oh, wait. Now India isn’t banning all crypto its government doesn’t create, it’s just going to tax the rest… and kind of ban it, maybe.

Was that hard to follow? Imagine what it’s like for the people living in those countries.

This month India’s crypto market capitulated when the powers the be said they were banning crypto.

From the Financial Times:

The announcement last month that India’s parliament would consider measures to “prohibit all private cryptocurrencies in India” sparked a frenzied sell-off, despite the same bill having been first floated earlier this year.

“What happened was panic,” said Nischal Shetty, co-founder and chief executive of crypto exchange WazirX. “And people who joined crypto in the last six to eight months were the ones who panicked most.” Prices on Indian exchanges temporarily slumped 10-15 per cent below the global market, he said.

It seems like India has the same idea as the UK here. Get regulators to try crush crypto then try to create your own CBDC instead. (More on that in a second.)

Again from the Financial Times:

While the details of India’s crypto bill are not known, it is expected to allow exceptions that “promote the underlying technology” of blockchain, a vast digital ledger, while ushering in a central bank-issued digital coin, according to the parliamentary agenda announcement.

It now looks like India is only sort of banning crypto.

From Coin Telegraph:

Indian news outlet NDTV reported on Thursday [4 December] that it had obtained details of a cabinet note circulating in the government regarding the proposed crypto bill.

NDTV reporter Sunil Prabhu said that the note contained suggestions to regulate cryptocurrencies as crypto assets, with the Securities and Exchange Board of India (SEBI) overseeing the regulation of local crypto exchanges.

According to Prabhu, investors will be given a specific time frame to declare their crypto holdings and transfer them to exchanges regulated by the SEBI, which suggests that private wallets may be banned.

Australia’s Central Bank hopes people will take its word for it when it tells them crypto is bad

Meanwhile, the head of Payments Policy at Australia’s central bank came out with this amazing piece of language. Have a read of it, and then I’ll translate it into real words:

I think there are plausible scenarios where a range of factors could come together to significantly challenge the current fervour for cryptocurrencies so that the current speculative demand could begin to reverse and much of the price increases of recent years could be unwound.

Households might be less influenced by fads and a fear of missing out [FOMO] and might start to pay more attention to the warnings of securities regulators and consumer protection agencies in many countries about the risks of investing in something with no issuer, no backing and highly uncertain value.

(Source: The Sydney Morning Herald)

Translation:

Crypto prices might drop. If they do, then people might finally listen to us when we tell them not to invest in crypto because it is bad.

Although, the message here is really quite clear (as much as doublespeak is used to dress it up):

People should stop thinking for themselves and go back to doing what we tell them.

Which brings us to the good ol’ US of A.

America is cracking down on stablecoins

As I write this, stablecoin issuers across the US are responding to a flurry of demands from the Senate Committee on Banking, Housing and Urban Affairs.

The Senate sent letters to:

Tether (USDT)

Circle (USDC)

Binance (BUSD)

Gemini (GUSD)

Paxos (Pax Dollar and DUSD)

TrustToken (TUSD)

And Coinbase (USDC)

Those links go to the Senate’s PDFs of the actual letters.

Here’s a sample of what they demand request:

The kicker here is that they ask for a response by the 3rd of December. So by the time you read this the Senate will probably already be reviewing what they’ve found out.

As the letters say, this comes in response to the President’s Working Group report on stablecoins that I reported on last month.

Basically, it’s not looking good for stablecoins right now, which could have a huge effect on the entire crypto market.

And it’s not only US regulators who are cracking down on stablecoins. It’s the EU, too.

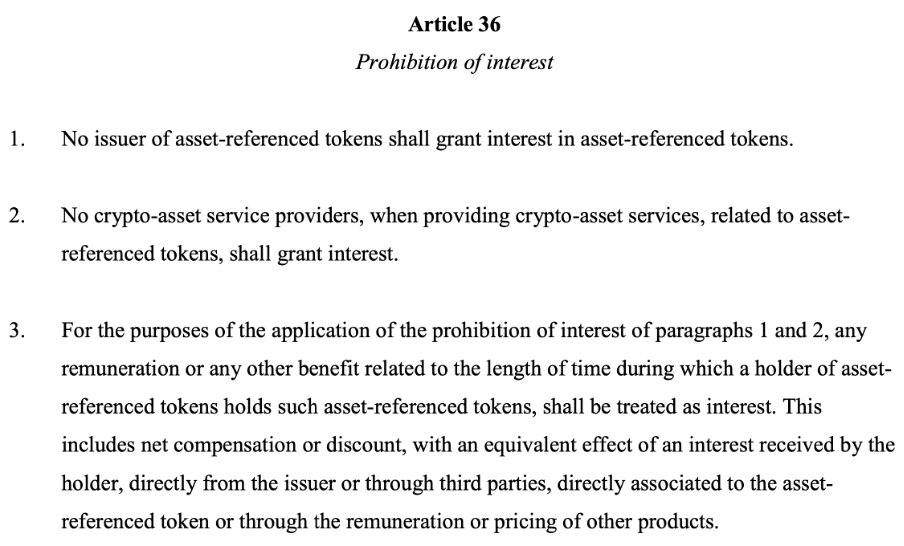

Europe releases its proposal for crypto regulation, and it’s surprisingly positive

On the 19th of November the Council of the European Union published its “Proposal for a Regulation of the European Parliament and of the Council on Markets in Crypto-assets”.

You can read it here.

But be warned, it’s about 405 pages long.

Thankfully for us, someone read it all and summarized it in this reddit post.

Here’s the summary of the summary, from the same post:

TL;DR: Cryptocurrency will still be the 'Wild West of Finance'; but now there will be a new Sheriff in town. And that Sheriff, is the European Union. It does no longer tolerate unregulated stablecoins; it does no longer tolerate shady projects with no utility, crappy white papers, and misleading marketing; and it sure as hell does no longer tolerate unprofessional exchanges who screw EU citizens out of their money. But it does like innovation and it will try not to hinder development in the cryptocurrency and blockchain space because they have made similar mistakes before in other industries.

It all seems remarkably positive. With one glaring exception: stablecoins. And especially earning interest on stablecoins.

From the proposal:

So it’s really not looking good for the likes of crypto.com, Celsius, BlockFi, Nexo et al.

We can’t have people making more than 0.01% interest on their savings, can we?

The banks would go out of business. No one would invest in stocks anymore. And negative interest rates couldn’t be used to force people to spend.

I’ve yet to see any kind of statement about this proposal and the banning of interest on stablecoins from any of the big centralised players I listed above.

But it kind of makes sense that they won’t be able to stay in business anymore, given that the US Securities Exchange Commission (SEC) bullied Coinbase into withdrawing its “earn” product earlier this year.

If you remember Coinbase was set to let all its customers earn 4% interest on its USDC stablecoin.

But the SEC said if the product ever launched it would sue. After a bit of very public back and forth, Coinbase eventually bent the knee.

While bowing down though, Coinbase did point out that tons of other massive companies already had the exact same product, and had been operating for years.

Celsius (which I use) for example, has over $26 billion locked up in its platform. And it’s already paid out almost $1 billion in interest.

Source: Celsius

Back in June, BlockFi had over $15 billion in assets, and that figure is likely a lot higher today.

And the other big names have similar amounts.

So if their business model gets made illegal, it’s not going to be pretty.

I’ll try reach out to some of the big names for comment for next month’s issue. But they are notoriously slow to respond to requests.

With all this stablecoin doom and gloom, there might still be light at the end of the tunnel.

That’s because decentralised stablecoins might not be covered by any of this proposed legislation. But it’s very hard to say.

A version of proposal dated the 9th of September 2020 specifically said algorithmic stablecoins (decentralised stablecoins) were exempt.

Source: EU

But in the latest version they seem to have changed their minds…

Source: EU

So… I dunno.

I think we’re just going to have to wait until all this starts getting picked up by bigger news sources and the EU and the companies involved will have to clarify things.

But if you have any money in stablecoins right now, it’s something to keep in mind.

While were here, I was planning to write this month’s premium issue on Terra Luna’s stablecoin, UST.

Using a DeFi platform made by Terra Luna itself, called Anchor Protocol, you can (in theory) make a steady 19.45% APY… which is absolutely crazy. But the more I look into it, the more it checks out.

That was until this coordinated stablecoin crackdown. Now I’m not so sure. So I’m putting that issue on the back burner and this month I’ll be doing a full review for my favourite crypto of all time, IOTA.

As you’ll see in the specific cryptos section of this piece, the timing for this review couldn’t be better.

IOTA has just completely reinvented itself and is set to launch two new cryptos this month… which you can only get by holding and staking IOTA.

And the best part is, the market doesn’t seem to have picked up on just how big of a deal these two projects could prove to be.

But I’m getting ahead of myself.

Because the biggest, baddest piece of regulation-related news is yet to come.

SEC Chair Gary Gensler wants all crypto exchanges to be regulated by the SEC, and most cryptos (it seems) classified as securities

And he’s going to sue anyone and anything that doesn’t agree.

Back in September, Gensler testified about crypto regulation before the Senate Banking Committee.

The outlook for crypto didn’t look good.

It seems Gensler has decided most cryptos are actually securities and that crypto exchanges should be regulated by the SEC as securities exchanges.

One of the committee members asked Gensler some follow-up questions, and he answered them yesterday (3rd of December).

As The Block Crypto reports:

Gensler argues that the SEC does not need to specify which crypto assets are and are not securities, as those laws and court cases established broad parameters — an attitude that has ruffled many in the crypto industry.

Following up on questions from the hearing, Toomey asked Gensler to "identify the specific characteristics that distinguish a cryptocurrency that is a security from one that has been deemed a commodity."

Gensler in turn cited those earlier laws, saying: "Thus it depends upon the particular facts and circumstances, whether any particular financial instrument, including a crypto asset, is being offered or sold as a security." He likewise avoided a question from Toomey that proposed a hypothetical dollar-backed stablecoin with reserves in FDIC-insured U.S. banks and asked whether that token would also be a security.

Regarding Gensler's responses, Toomey said: “Chairman Gensler’s failure to provide clear rules of the road for cryptocurrencies underscores the need for Congress to act.”

So basically… a crypto is a security if we say it’s a security.

The only cryptos we know are exempt from this are Bitcoin and Ethereum, which are already classed as commodities.

The rest, it seems, could all be in the firing line.

On Friday, share prices in the two major US-listed crypto exchanges, Coinbase and Bakkt both fell around 6.7%.

The only real hope here is that Ripple wins its ongoing case with the SEC.

If Ripple wins it will set a precedent for crypto not being a security. If it loses… well. It won’t be good.

Right now, according to Ripple’s CEO, they’re “seeing pretty good progress, despite a slow-moving judicial process.”

He expects the case to reach a conclusion in 2022. And he seems optimistic about the outcome:

“Clearly we’re seeing good questions asked by the judge. And I think the judge realizes this is not just about Ripple, this will have broader implications,” he said.

In the meantime…

The CEOs of America’s biggest crypto businesses will testify before Congress on the 8th of December

They’ll be witnesses at the hearing on Digital Assets and the Future of Finance: Understanding the Challenges and Benefits of Financial Innovation in the United States.

The six CEOs on the list are:

· Jeremy Allaire, CEO, Circle

· Sam Bankman-Fried, CEO, FTX

· Brian Brooks, CEO, Bitfury

· Chad Cascarilla, CEO, Paxos

· Denelle Dixon, CEO, Stellar Development Foundation

· Alesia Haas, CEO, Coinbase

You can watch the hearing live, if you want, here.

(It’ll take place this Wednesday at 3pm UK time.)

Maybe things will go well. Who knows?

I mean, it’s not all doom and gloom.

Wyoming is definitely backing crypto’s corner.

Wyoming wants Kraken to get its banking charter already – and it’s willing to fight the Fed for it

Remember when top US crypto exchange Kraken got a banking charter in Wyoming back in September 2020? I covered it here.

Well, a year later it’s still waiting on the paperwork. And Wyoming isn’t happy about it.

This week Cynthia Lummis, serving as the junior United States senator from Wyoming wrote an op-ed in the Wall Street Journal calling out the Fed and the people who run it.

From the piece:

Over the past year my faith in the Fed has been deeply shaken by its political approach to digital assets in my home state, Wyoming, greatly contributing to my concerns over President Biden’s nominees, Jay Powell and Lael Brainard.

She goes on to say that since 2019 Wyoming has been working on banking charters for crypto. They held over 100 meetings with the Board of Governors and Federal Reserve Bank of Kansas City.

Everyone agreed the banking charters were legit, and in 2020 Wyoming granted them to two companies, Kraken and Avanti.

However, “the Fed doesn’t seem to care.”

It’s been more than a year and the Fed still hasn’t even started processing the applications.

Lummis continues:

The Fed is violating the law by delaying. In 1994 Congress required the Fed to act on all applications within one year. Numerous federal courts have stated that the Fed has a duty to give payment system access to all banks and credit unions conducting legal activities. The Fed itself has said its payment services will be available “to all depository institutions on an equitable basis . . . in an atmosphere of competitive fairness.”

In this light, I am deeply concerned about the nominations of Chairman Powell and Gov. Brainard, who helped helm the Fed as it took these questionable actions.

…

The Fed’s lack of responsiveness is becoming a trend. Recently, the central bank thumbed its nose at Sen. Pat Toomey’s request for its research into climate and equity.

As the Senate considers Mr. Powell’s and Ms. Brainard’s nominations, they must address these concerns. The American people expect them to follow the law without bias or delay. Anything less makes them unworthy to serve.

The upshot is Lummis is, “likely to vote against President Biden’s nominees to head the U.S. Federal Reserve, and will rally other senators against them,” according to her aide quoted in CoinDesk.

So there are people in high places who support crypto innovation. And they are fighting crypto’s corner. The issue is there are people in even higher places who hate crypto.

In the end, progress and technology will always win, as it always has.

But who can say how long the battle will last?

Thankfully, it looks like the war is already won in Canada.

Royal Bank of Canada bigs up blockchain

While the Royal Bank of Canada isn’t Canada’s Central Bank, it’s still a bigshot commercial bank.

And it seems pretty impressed with crypto’s potential.

From CoinDesk:

Blockchain technology has evolved enough to meet the critical demands of at “least certain segments in the banking and financial markets,” according to a research note by the Royal Bank of Canada (RBC).

Blockchain offers distinct value propositions: “displacing trust with truth; real-time bilateral settlements; real-time servicing; enhanced security; automation; the ability to operate 24/7/365.”

However, that’s not the biggest development on the Canadian crypto scene this month. Far from it.

$4.2 trillion asset manager, Fidelity launches real Bitcoin ETF in Canada

This week also saw Fidelity – the 4th biggest asset manager on the planet, with more than $4.2 TRILLION under management – launch a Bitcoin ETF in Canada.

And not just any Bitcoin ETF, but a spot Bitcoin ETF.

That means the ETF actually buys and holds real Bitcoin, not a synthetic derivative like the ETFs that were approved in the US.

This is some of the biggest adoption the world of crypto has ever seen.

One of the biggest and most reputable asset managers in the world launching a real Bitcoin ETF in a well-established financial market would have been unthinkable, even just a few years ago.

UK regulators still refuse to let citizens invest in Bitcoin ETFs – for your own safety

In the UK it would still be unthinkable as the Financial Conduct Authority won’t let any UK citizens invest in any regulated crypto investments.

So, unfortunately, if you’re reading this in the UK, you can’t invest in the Fidelity Bitcoin ETF. It would be illegal.

But for the rest of the world, this is a big deal.

As the Financial Times reports:

The Fidelity Advantage Bitcoin ETF (FBTC) is designed to invest in “physical” spot bitcoin, a model the US Securities and Exchange Commission has so far rejected, rather than bitcoin futures contracts, which the US financial regulator has permitted.

The entry of the world’s fourth-largest fund manager, with assets of $4.2tn, into the crypto market will, though, be seen as a further sign of the growing acceptance of digital currencies in the traditional investment world.

The top two comments on that piece perfectly sum up my thinking on the topic:

And on that note, it seems that maybe the (notoriously anti-crypto) Financial Times is finally seeing the writing on the wall with the UK’s crypto policies.

Is the Financial Times finally coming round to crypto?

On the 3rd of November, it published an article with the following headline:

UK crypto derivatives ban fails to protect retail investors

Regulators need to take a more flexible approach

I never thought I’d see that in the FT.

From the article:

The FCA derivatives ban seems strangely misaligned with the UK’s historical successes as a fintech hub and the government’s commitment to be a competitive and innovative jurisdiction for financial services. Even in the EU, often seen in Britain as a bureaucratic monster slow to keep up with financial pioneering, there are no similar bans. Nor in the US or most of Asia.

Last week’s move by the US authorities only emphasises how isolated Britain risks becoming. In fact, the US Commodity Futures Trading Commission, has been overseeing regulated crypto derivatives markets for nearly three years with products that offer a reliable basis for valuation. These markets are accessible to retail as well as professional investors.

And again, some of the top-rated comments perfectly reflect my views on this situation:

Here’s a link to that link, if you want to read it.

And here’s a very interesting excerpt from that report:

A key theme in responses we received to the CfI was the need to further segment high-risk investments from the mainstream market, and to further disrupt consumers from investing in inappropriate investments that do not meet their needs.

Wow.

So it looks like the plan is to, “further disrupt consumers from investing in inappropriate investments that do not meet their needs.”

Meanwhile, as I’ve just said, Fidelity is literally launching an ETF in Canada to let people get safe, easy access to these “inappropriate investments”.

Looks like no one told the Bank of England regulated crypto products are banned in the UK

On the topic of regulatory madness…

A new statement just came out saying the UK could get a CBDC before 2030.

From the Bank of England statement:

In April 2021, the Bank and HMT initiated the joint CBDC Taskforce to coordinate the exploration of a potential UK CBDC. The Bank also set up the Engagement and Technology forums, where relevant stakeholders from industry, civil society and academia provide strategic and technical input to the work on CBDC.

The 2022 consultation will inform a decision on whether the authorities are content to move into a ‘development’ phase which will span several years. A technical specification would follow the consultation explaining the proposed conceptual architecture for any CBDC. This could involve in-depth testing of the optimal design for, and feasibility of, a UK CBDC.

If the results of this ‘development’ phase conclude that the case for CBDC is made, and that it is operationally and technologically robust, then the earliest date for launch of a UK CBDC would be in the second half of the decade.

Given that a CBDC by definition would be a cryptocurrency, then any kind of regulated investments that use it would fall under the FCAs ban. So basically every investment you can currently buy or trade with GBP.

How is that going to play out?

Will we see the Governor of the Bank of England being sued by the FCA and send to jail?

Wouldn’t that be one for the history books.

It’s like being back in the Middle Ages

All of this reminds me of the crazy situation the church found itself in towards the end of the Middle Ages.

(I’ve spent most of the last month reading Bertrand Russell’s History of Western Philosophy… if you were wondering why we’ve taken this strange turn.)

Back then everyone in power was just making up their own rules about how things should be run.

Different sides elected different popes, and eventually there were three popes – one of whom was an ex-pirate. No one knew who to follow or what was going on.

From Bertrand Russell’s History of Western Philosophy:

Thus began the Great Schism, which lasted for some forty years. France, of course, recognized the Avignon Pope, and the enemies of France recognized the Roman Pope. Scotland was the enemy of England, and England of France; therefore Scotland recognized the Avignon Pope.

Each pope chose cardinals from among his own partisans, and when either died his cardinals quickly elected another. Thus there was no way of healing the schism except by bringing to bear some power superior to both popes. It was clear that one of them must be legitimate, therefore a power superior to a legitimate pope had to be found.

The only solution lay in a General Council. The University of Paris, led by Gerson, developed a new theory, giving powers of initiative to a Council. The lay sovereigns, to whom the schism was inconvenient, lent their support. At last, in 1409, a Council was summoned, and met at Pisa.

It failed, however, in a ridiculous manner. It declared both popes deposed for heresy and schism, and elected a third, who promptly died; but his cardinals elected as his successor an ex-pirate named Baldassare Cossa, who took the name of John XXIII.

Thus the net result was that there were three popes instead of two, the conciliar pope being a notorious ruffian. At this stage, the situation seemed more hopeless than ever.

That ridiculous state of affairs is what crypto regulation feels like today.

You have Canada and Europe pushing innovation, letting their citizens think for themselves, and, I would imagine, setting themselves up to win the future.

You have the USA somewhere in the middle… it could go either way. And we’ll get a good idea of which way it will go in the coming weeks and months.

Then you have China, India and the UK at the complete opposite end.

China wants to control everything and shut down anything that could put its rulers’ personal power in jeopardy.

India doesn’t really seem to know what it wants yet.

And the UK wants to keep its old boys’ club in business for as long as it can… who cares about future generations?

The pope, the anti-pope and the pirate. But who’s who?

Could Europe or Canada overtake the US as the tech capital of the world?

If we play all of this out to its logical conclusion, we could end up with the US being eclipsed by Europe and/or Canada as the tech capital of the world.

Remember, Europe’s proposed crypto legislation is pro innovation and very pro crypto in general. The only thing it doesn’t like is interest on stablecoins.

Meanwhile the US, which won the tech race of the 90s and 2000s, is balancing on a knife-edge.

If it goes heavy handed with regulation, all the crypto businesses will simply move countries… probably to somewhere in Europe (or Singapore. There is a lot of crypto innovation in Singapore) or maybe Canada.

Remember, crypto is a global phenomenon. Moving operations around the globe isn’t hard… as we saw when China last banned it.

Obviously many in the US know this and they are fighting crypto’s corner. But the US also has super powerful lobbyists in the traditional financial world. So the pro-crypto people might not win.

The UK? Frankly, it doesn’t even count. Its already made its bed and is happy to lie in it.

What does all this mean for people like us?

Well, crypto isn’t going anywhere. Although many people in traditional tech and finance don’t see it yet, crypto will eat everything.

(And to be fair, a lot of them already acknowledge this.)

There will be stumbling blocks along the way. There will be regulatory crackdowns. And there will be more market crashes – just like the one I’m seeing as I type this.

But crypto is the future. And ultimately, you can’t stop the future.

Wow. We really went down the rabbit hole there, didn’t we?

Okay, I’ve completely run out of time for this month’s issue. So I’m just going to link to the stories I was going to write commentary about.

Other things that are happening

Evergrande and pals are still wreaking havoc

From the Wall Street Journal:

What began early this summer as a confidence crisis around industry giant China Evergrande Group has spread to numerous real-estate firms that are now at much higher risk of reneging on their debt. At least four developers have defaulted on dollar bonds since September.

From this Friday’s morning briefing in The Economist:

Bakkt flies and falls

Mastercard makes a deal with Bakkt (remember Bakkt?). Rumours circulate that Bakkt might be working with Apple, too. Bakkt becomes a new memestock and jumps 300%. Omicron hits. Crypto regulation hits. Bakkt falls 70%. Ouch.

Source: Yahoo! Finance

Apple CEO says he invests in crypto – but has no plans for Apple itself to get involved

From CNBC:

Apple CEO Tim Cook said he personally owns cryptocurrency after he was asked at The New York Times DealBook conference if he owns bitcoin or Ethereum.

“I do. I think it’s reasonable to own it as part of a diversified portfolio,” Cook told Andrew Ross Sorkin in an interview that aired Tuesday. “I’m not giving anyone investment advice by the way.”

Cook said that he had been interested in cryptocurrency “for a while” and that he had been researching the topic.

The Mt Gox saga continues – 141,686 Bitcoin could be flooding the market any day now… maybe that’s what caused this weekend’s crash

Back in 2018, the Mt Gox hack, and subsequent court case was credited with causing, or at least initiating, the crypto winter.

I wrote a big essay all about it. I would link to it here, but it’s no longer hosted by Southbank Research.

(If this latest Mt Gox development turns out to be the cause of this week’s crypto crash, I’ll republish it on coin confidential and link to it in next month’s issue.)

Anyway. The saga continues. But for some reason, no one seems to be talking about it. And they definitely should be.

Basically back in 2014 Mt Gox was the biggest exchange in the world. It got hacked and pretty much everyone lost pretty much everything.

It would be like Binance or Coinbase losing everything today.

Eventually a lot of the funds were recovered. And there’s been an ongoing court case ever since to decide where those funds should go.

The court case now appears to have reached a conclusion, and 141K bitcoin, worth around $6.5 billion (even after today’s crash) will be making their way to the people who originally owned them.

Here’s Coin Journal’s coverage of it.

What will all those people do with their $6.5 billion Bitcoin? Well, if they decided to cash out – and who could blame them after waiting seven years for their money – it could tank crypto markets.

Interesting timing, given this week’s market movements.

Spanish banking giant Santander to offer crypto ETFs

I told you Europe was doing well on the crypto front, didn’t I?

From Coin Corner:

Santander does not want to miss out on the bitcoin boom and other cryptographic projects either. The Spanish bank is finally betting on the Blockchain revolution through funds referenced to bitcoin and, perhaps, to other major cryptocurrencies. These ETFs will most likely be futures ETFs, which does not involve buying bitcoin or cryptocurrencies, to back the fund, in the style of the two ETFs (ProShares and Valkyrie) that have recently been approved in the US.

The strong demand from Santander customers to invest in bitcoin seems to have played a role in the bank’s decision. However, Santander was not the first major Spanish bank to facilitate investment in cryptoassets. Since last June, BBVA has already had a bitcoin trading and custody system in operation, albeit exclusively through its subsidiary in Switzerland, where legislation on cryptoassets is clearer and more advanced.

Santander is thus following in the footsteps of investment banks such as BNY Mellon, Morgan Stanley, Goldman Sachs, JP Morgan and investment funds such as BlackRock.

Square changes name to Block and plans to launch a Decentralised Bitcoin Exchange

This week Twitter founder and CEO Jack Dorsey left Twitter.

Word on the street is he wants to dedicate more of his time to crypto, and bitcoin in particular.

He also owns Square, which is a payments platform with crypto buying features.

Soon after Jack stepped down, Square announced it was changing its name to Block. You know, as in blockchain.

Block already announced plans to launch a decentralised Bitcoin exchange back when it was still hip to be Square.

So it looks like we could see another major player in the US crypto space. I wonder how Jack is feeling about the regulatory crackdown.

Specific crypto news

Bitcoin undergoes Taproot upgrade

This month Bitcoin underwent its first proper upgrade in four years.

The upgrade is called Taproot, and it’s kind of hard to find out what it actually does.

Apparently, it will make Bitcoin more private.

From Ledger Insights:

For Bitcoin, Taproot improvements are multifold. The first one is anonymity. With Taproot, your keys have less chain exposure. A Bitcoin mining engineer, Brandon Arvanaghi, said that with this upgrade, “you can kind of hide who you are a little bit better.”

But what’s the point of being “more private”? You’re either a private crypto like Monero, or you’re not. People can still trace your Bitcoin transaction, even after Taproot.

The other big thing is that Taproot is supposed to sort of enable smart contracts for Bitcoin.

But again, it doesn’t really. It just makes smart contract side chains and other layer twos easier to connect to the Bitcoin network (like lightening network).

There still won’t be smart contracts on Bitcoin’s main chain.

I guess that’s why Bitcoin’s price didn’t really move on the news.

Solana has been busy

Everyone’s favourite crypto to hate, Solana, has been very busy this month.

(I don’t hate Solana. It’s just become so big that it’s now drawn the ire of people who didn’t invest in it when it was small. Read my Solana review here.)

Here are a few of the big ones:

Brave partners with Solana to integrate it into the browser and make it the default for DApp support

Reddit co-founder, Solana venture team up on $100m blockchain investment initiative

FTX, Lightspeed, Solana Ventures to Invest $100M in Web 3 Gaming

Blockchain streaming platform Audius announces Solana NFT integration

Algorand has been busy

Shamelessly stolen from this Reddit post:

Decipher, Algorand's major conference, is currently underway. There, Gary Malouf, Head of Engineering at Algorand, and Rotem Hemo, Director of Product Management at Algorand, just announced that state proofs will come to Algorand in early 2022. With stateproofs, Algorand will be the first blockchain to provide a post-quantum security solution. On the roadmap are post-quantum secure catchup (integrating state proofs in to the catch-up process), zk-SNARK proofs (efficient and cheap verification of state proofs) and light clients (tools to help entities use state proofs). So your transactions will live forever on the blockchain.

Other exciting news in my opinion were:

Francis Suarez, 43rd Mayor of Miami, has agreed to receive every other paycheck in Algo

Hivemind, a $1.5 billion venture to institutionalize crypto investing, has selected Algorand as a strategic partner

Moreover, bank-issued stablecoins ("Digital Deposit Receipts") will come to Algorand and Ethereum. VCAD was minted yesterday on the Algorand mainnet. US Dollar version will follow.

AXA XL, the U.S. subsidiary of AXA S.A., the world's third-largest insurer, is working with Algorand on an art insurance platform (money for your art)

One of the world's leading manufacturers/retailers will introduce a first-of-its-kind Buy Now, Pay Later platform on Algorand

1&1 is working on a digital-asset exchange and commerce engine that will create fungibility across cryptocurrencies, loyalty points, rewards, and fiat currencies

Mina Protocol board member announced as head of crypto Twitter

Tess Rinearson serves on the board of the Mina foundation. This month she was appointed as the engineering lead of “all things blockchain at twitter”.

Could we see a Mina/Twitter partnership? Who knows. Probably not. But if it ever did happen… boy, would that be big for Mina.

IOTA is completely reinventing itself

I already mentioned this earlier. But basically IOTA is launching two new projects:

A fully functioning testnet called Shimmer that will get all of IOTA’s newest innovations first, in order to test them out in the real world (Like Polkadot’s Kusama, which is currently worth $2.6 billion).

And a new smart-contract network called Assembly. This is basically IOTA’s version of Ethereum… but faster and with the option for zero-fee smart contracts. Oh, and those smart contracts will be atomically composable, like Radix.

Now for the really crazy part. The only way to get these new networks’ tokens is by staking IOTA.

Yes, if you own IOTA you can stake it for 90 days and get free Shimmer and Assembly tokens.

Staking isn’t live yet. It’s going to launch this month, and IOTA will give people 24 hours’ notice before it goes live.

Here’s a link to IOTA’s official shimmer website.

And here’s a link to IOTA’s official Assembly website.

There is a lot of information on both of those sites if you want to read up.

I’ll be reviewing IOTA in this month’s premium issue

In light of these developments – and because I’m always writing about IOTA without giving it a proper review – I’m reviewing IOTA for this month’s premium issue.

I plan to release the review on Boxing Day.

So if you’re already a premium member, you can read it during some Christmas downtime.

And if you’re not a premium member, you can join here.

When you join, you’ll also get instant access to my full archive of in-depth crypto reviews, which includes Solana, Polkadot, Algorand, Radix, Mina Protocol and Fantom.

Okay, that’s all for this month.

Let’s hope the crash doesn’t last too long.

Thanks for reading.

Harry

Subscribe for exclusive content

The best newsletter in crypto, or your money back (it's free).

.jpg){kind=link}

{kind=link}